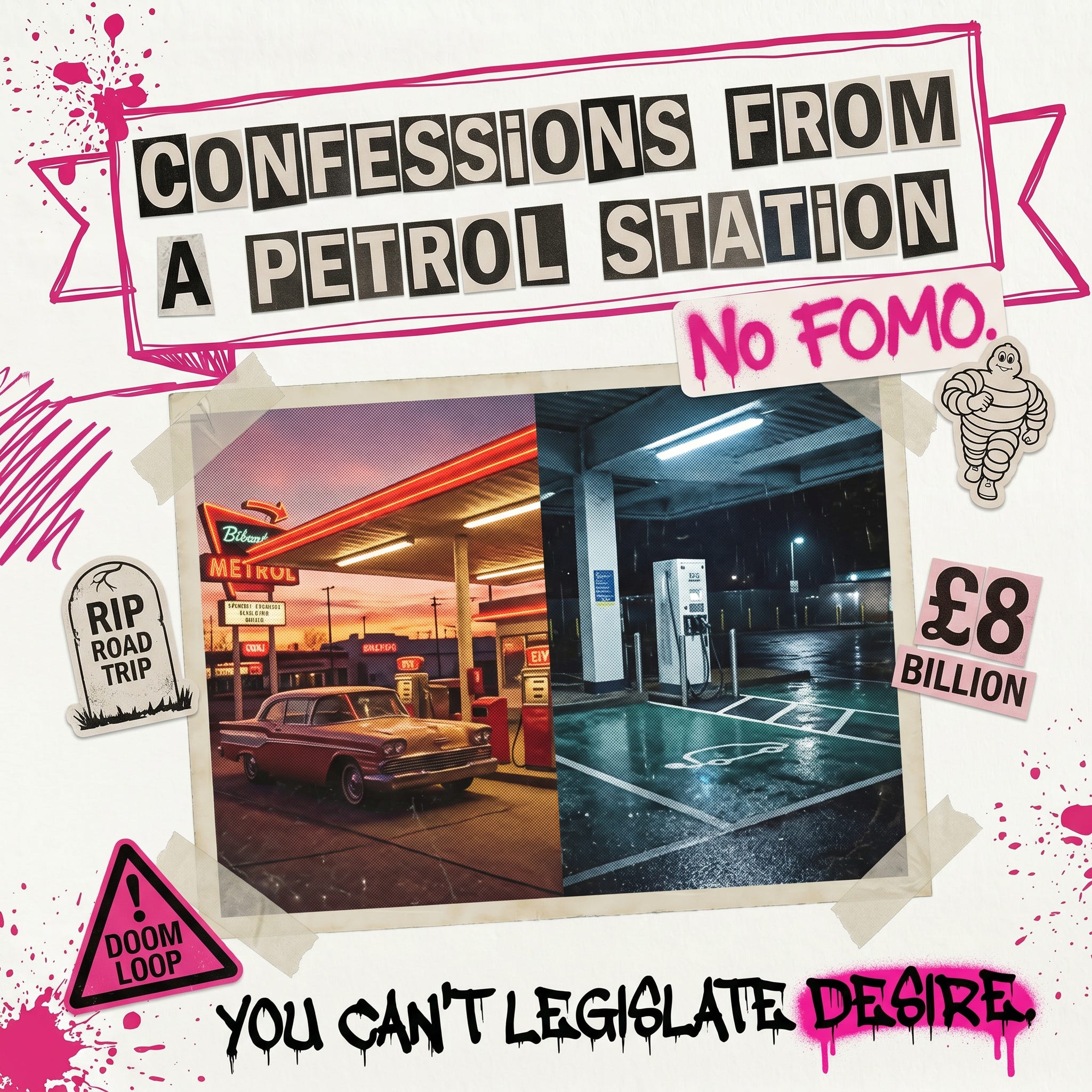

confessions from a petrol station

I don't have an EV, and and I don't have FOMO. This is a problem.

Welcome to the anarchists who have joined (and thank you for the external validation). If you’re new and like what you’re reading, check out our manifesto, the tenets of good energy policy, or why I think the UK is screwed.

I drove home from France on Sunday. Fourteen hours, a Land Rover, two dogs in the back. The puppy is ten months old, which means a stop every 2-2.5 hours. I saw nearly every service station and most of the aires between Hossegor and London.

Somewhere around hour eight, I was eating a(nother) baguette beside the EV chargepoints and it occurred to me that I have zero FOMO about not owning an EV.

I should drive an EV. I work in energy. I opine about decarbonisation. I’ve sold a shit-tonne (technical measure) of residential EV chargers.

I know the benefits and the savings maths inside and out. I’ve worked at four companies with EV salary sacrifice schemes. One even actually leased EVs. I’m just… indifferent. Not hostile, but unmoved.

I live in central London, which means I rarely drive. The few times I do, it’s this kind of trip: long-distance and motorway-heavy. We own our car and have no payments, so there’s no burning incentive to switch.

If I commuted, I’d probably have one. The savings’ maths definitely math for daily use and I could have a home charger. Even public charging is cheaper than petrol now and there’s no end in sight re: Iran. But it would be a change driven by logic, not desire.

[One valid barrier: I hate touchscreens in cars (people with nails know) and EVs are riddled with them. I’m firmly on Team ‘Bring Back Buttons’, with Captain Jony Ive. 🫡]

I’ve looked, but there’s no killer EV for me. Nothing that I want to drive. Most cars look the same. If I was commuting every day, I’d likely have a MINI Cooper because it has personality. (I was genuinely interested in the electric Porsche Boxster, but RIP.)

Cars have unlocked personal freedom, given us iconic marketing, and defined 126 years of dining recommendations. But why does this transition feel less like the rise of an exciting future and more like a begrudging inevitability?

is the infrastructure dying?

Recently, EO Charging entered administration. PwC was appointed, 69 of 93 employees were made redundant, and an accelerated sale process failed to find a buyer.

It is not an isolated event. Reporting for the Forecourt Trader, Hugo Griffiths observed that “Losses in the chargepoint sector are the rule, not the exception.”

In 2024, Fastned’s UK arm, Osprey Charging, Blink Charging, and Char.gy all posted losses between £5 to £10 million. In 2025, Gridserve lost over £80 million while InstaVolt lost £8.5 million, an improvement on the £15.6 million it lost the year before. Even the majors can’t make it work: BP Pulse lost £66.4m in 2024, while Shell EV Charging Solutions lost £8.4 million.

The reason is partly structural and partly absurd. Structurally: infrastructure has a J-curve cash profile, so losses are to be expected for a time.

Absurdly: UK rules changed in 2023 to base charges on the size of the connection rather than the power actually used. Osprey reported one site where annual standing charges jumped from £87 to £33,651, a 38,579% increase.

Translation: the faster you build, the faster you go broke. Another fabulous example of the hypocrisy of UK energy policy.

(There’s a separate layer to this: public charging is taxed at 20% VAT while home charging is taxed at 5%, meaning the third of UK households without driveways pay a structural penalty for being poorer or living in flats.)

“but EV sales are up”

Yes. New EV registrations in the UK hit a record in March 2026, and full battery-electric vehicles now make up roughly a quarter of new car sales.

The headline growth is real, but it’s heavily fleet-driven, propped up by salary sacrifice schemes, and underwritten by a ZEV mandate that fines manufacturers who don’t sell enough EVs.

We must consider the public price tag. The UK has committed roughly £8 billion in direct EV subsidies — vehicle grants, charging grants, manufacturing support, infrastructure funds — plus roughly £5-6 billion a year in ongoing tax expenditure on salary sacrifice and Benefit-in-Kind exemptions.

Strip the policy scaffolding out and the retail demand picture looks more wobbly. While the growth is impressive, and the global transition has apparently reached a tipping point, carmakers still took a $50 billion loss on EVs.

For now, the relevant point is this: even with a mandated demand floor and £8 billion in direct subsidies, the folks building the charging infrastructure are still going broke.

graveyards with intermittent visitors

According to Zapmap, the average UK public charger is used 11% of the time. Rapid and ultra-rapid chargers — the expensive ones, with the worst standing-charge exposure — handle roughly four sessions a day, averaging 37 minutes each. (McKinsey reckons public charging needs around 20% utilisation to be profitable.)

There are now considerably more EV charge points than fuel pumps in the UK, but this isn’t Field of Dreams. They don’t come just because you’ve built it. Imagine a hotel running on 11% occupancy. Death sentence.

The infrastructure is going broke because utilisation is too low. Utilisation is too low because not enough people are buying EVs. Not enough people are buying EVs because they’re worried about charging infrastructure. The charging infrastructure is going broke because…

You see the problem. New petrol and diesel car sales are banned from 2030, and we’re in a doom loop.

We keep trying to subsidise our way out of this, but the only way out of a doom loop is from the outside. Demand follows desire, not subsidies.

Take a quick look back at history and you’ll realise we’ve seen this before. Purpose-built petrol stations started popping up in the 1940s, peaked in the early 1980s and have been declining ever since.

The 1970s energy crises pushed margins to the point where service station owners stopped selling fuel altogether because vehicle maintenance was more profitable than the pumps. Then American retailing giants J.C. Penney and K-Mart fell. They had the scale, the locations, and the customers, but fuel margins were too thin to compete.

All three of the now-top operators — Southland (7-Eleven’s parent), Circle K, and NCS — entered bankruptcy in 1991. They survived only by restructuring around the same model: convenience stores.

It took the industry over 40 years, but they finally figured it out:

it’s never about petrol

Ask anyone who has ever run a forecourt — Shell, BP, PetroCanada, Couche-Tard, the people behind every Buc-ee’s in Texas — and they’ll tell you the same thing. The actual business is coffee, sandwiches, lottery tickets, chocolate bars, energy drinks, hot food, and clean toilets.

Margins on petrol are 2-5p per litre. Margins on a flat white and a pastry are 60%.

Buc-ee’s became a cultural phenomenon because of BBQ sandwiches and famously clean bathrooms, not because of the pumps. This is, at its core, a retail hospitality business.

Now look at who’s building EV charging.

The CEO of InstaVolt spent 26 years in energy services and energy efficiency. The chairman co-founded an energy efficiency firm. The CFO came from Vauxhall and Vodafone. The largest shareholders sit on the board having previously worked in infrastructure private equity, with portfolios in fibre networks and power generation. There is exactly one retail veteran on the entire board — the ex-Tesco and Morrisons CFO — and he joined as a non-exec in 2022.

This isn’t a criticism of any individual. These are capable people who’ve spent their careers thinking about networks, throughput, and yield. They’re running EV charging as if the goal were laying cable. It isn’t.

The goal is delighting someone with a Tesla and 25 minutes spare so they come back next week.

The capital structure reinforces this. Infrastructure private equity and pension fund debt are the cheapest money available, but you don’t build Buc-ee’s with infrastructure debt. You build a substation, so we are getting substations: sited where the grid connection is cheap, optimised for kW delivered, marketed on reliability and speed.

Nobody has ever fallen in love with a substation. A Buc-ee’s sandwich, however? Lust.

It harkens back to Rory Sutherland’s “make the train journey more desirable rather than faster“ example: “If you give engineers a problem, they will define it in terms that are most amenable to being solved by engineering.”

To be fair, the valid difference in EV charging is that it’s possible to embed charging infrastructure within the fabric of a community. But those efforts are struggling too.

A few operators have spotted the problem. BP converted a filling station forecourt with an M&S Food Store and a coffee shop to EV-only charging, and reported that they are hitting utilisation rates that weren’t expected until 2030.

Fastned runs flagship sites in Belgium with restaurants, outdoor play areas, and ‘nature-inspired’ solar canopies. Gridserve has built the UK’s most ambitious electric forecourt at Braintree with meeting pods, kids’ zones, EV Gurus, even puppuccinos.

They are thinking differently. They are also losing money — Fastned €27m last year, Gridserve £80m. The question is: can they hang on until enough people buy EVs?

V2G, or: the same mistake one layer deeper

A brief detour, because this is not exclusive to public charging.

Vehicle-to-grid is the idea that EVs can sell electricity back to the grid at peak times, turning your car into a mobile battery. It’s often pitched as the demand unlock for EVs: buy the car, earn yield from the car, fall in love with the car.

Because everyone’s chasing that “Paradise By the Arbitrage Potential.”

V2G is the same category error as charging infrastructure, displaced one layer further into the system. The people building it think the transition is a yield curve problem.

Sigh.

you can’t legislate desire

The 20th century didn’t make people fall in love with cars by mandating them.

It built Route 66, the drive-in, the Michelin Guide, the road trip movie, the Cars franchise that made an entire generation of children car-fluent. Modern hospitality is, in large part, a century of infrastructure invented to give drivers reasons to stop.

Somewhere in the EV transition, we’ve forgotten that the car is a vehicle for belonging, not transport. We’re trying to swap the engine and pretend that everything else is identical. That’s a substitution, not a transition. Substitutions aren’t sexy.

(You know what is sexy? Something that’s banned. We’ve learned nothing from Prohibition.)

There’s an argument that the car itself is losing its place in society. But in an era when train journeys are ridiculously expensive and people are questioning the ethics of flying, this should be fertile ground to re-energise (pardon the pun) the road trip.

But wait, you gasp. THE RANGE ANXIETY. The research says people have range anxiety, so the advertising focuses on range anxiety, which reinforces that range anxiety exists.

Do you know how many times I’ve run out of petrol? Plenty. Fuel gauges used to be vague approximations, and I was broke. (Once, famously, when I picked my ex-husband up from the airport. It wasn’t the reason for the divorce, but it was probably a contributing factor.)

I don’t have “petrol anxiety.” I still play gas tank roulette.

Hitting 0% charge is a bigger deal than running out of gas, but I also know that logic has no chance when faced with emotional longing.

Rather than fearing long distances, EVs could unlock guilt-free travelling, with charging infrastructure that leads you to experiential destinations. Range shouldn’t matter, because there are gorgeous, entertaining, or delicious stops every couple of hours anyway. (I mean, we’re already starting to electrify Route 66.)

Or, do we need a resurgence of the motoring club, à la the Royal Automobile Club? RAC patrolmen used to salute members as they drove past. They had RAC-specific roadside assistance boxes (members had keys) and also introduced star-based hotel rating systems alongside the AA in the early 20th century.

(France rated food, Britain rated hotels. Read into that what you will.)

This is what I’m pondering: what would make me feel like I’m genuinely missing something by not having an EV?

I’ve made energy policy my lane, but policy can’t save us here. The transition needs cars worthy of desire and charging worth visiting. This is a creative problem, not a policy problem.

I’ve been working on a multi-part series to explore:

Part two: how the car actually won, and what we can steal from a hundred years of motoring culture

Part three: winners & losers — Norway, China, and cautionary tales of policy without demand

Part four: a vision of what a desire-led approach means for infrastructure

For now, the question that started this.

The infrastructure is dying for lack of people. The people are missing for lack of confidence. The confidence is missing for lack of desire.

What do drivers desire?

📚 recommended reading

If you’re an EV nerd in the UK, The Fast Charge by Tom Riley is a must-subscribe.

Love the idea of looking at this from the POV of desire - and essentially, marketing. I’d take it one step further and say we also need Identity. It doesn’t matter how many cool features a Tesla has if the company is associated with pure loser energy. It’s fascinating to me that EVs have become adjacent conceptually to the manosphere… prob impacting adoption too. One for the next article, please? 🙏