Ed Miliband is right. And we're screwed.

The UK is building the right future, but it may not survive the next decade.

Welcome to the anarchists who have joined (and thank you for the external validation). If you’re new and like what you’re reading, check out the manifesto and the tenets of good energy policy.

The OECD confirmed what anyone paying attention already knew: the UK is the most exposed advanced economy to energy price volatility.

Not among the most exposed. The most exposed.

The Strait of Hormuz crisis made this concrete. Once again, the UK energy market is working exactly as it was designed.

how we got here

The UK’s energy vulnerability isn’t a single policy failure. It’s a structural condition built up over thirty years of decisions that were each, individually, defensible and collectively, catastrophic.

Here are the high (low?) points.

Supply.

North Sea gas production peaked around 2000 and has been in decline ever since (partly geological, partly political, partly economical).

The UK went from net exporter to net importer in less than a decade and as usual, responded with vague hand-waving that “the market will sort it.”

In a surprise to absolutely no one: markets optimise for cost, not resilience. (See also: privatisation of UK water.)

The result: significant dependence on LNG imports and pipeline gas from Norway and continental Europe. Most buffer this import risk by building ample strategic storage.

The UK has chosen an, err, different approach.

Infrastructure.

The UK has 90-days worth of oil reserves, which is an IEA requirement for net-importing countries.

The gas storage capacity is embarrassing and irresponsible. We still act like an exporter. We have about ~3 bcm of storage, which could equate to 10-13 days of winter demand in the best possible operating conditions.

Comparatively, Germany holds ~90-days.

When Centrica closed the Rough (~3.3 bcm) storage facility in 2017, there wasn’t a move to replace it because there’s was a belief that interconnectors and spot markets could substitute for storage. They can, when times are good. They cannot when (1) every European country is pulling on the same system simultaneously, and (2) gas tankers are paralysed in the Middle East.

This is not a theoretical risk. It happened in 2021. It’s happening again, RIGHT NOW.

Japan and South Korea have zero pipeline connections and are entirely dependent on LNG tankers arriving continuously.

Japan holds the world’s largest LNG storage capacity; South Korea the second largest.

Both governments treat storage as the direct corollary of import dependence, a lesson the UK has failed to internalise.

Market design.

UK electricity is priced at the margin. The last unit of power dispatched sets the price for everyone. In the UK, that marginal unit is a gas-fired generator between 15-49% of the time.

This means that when gas prices spike, electricity prices spike, regardless of how much of the grid is running on wind and solar.

In a system where 60% of generation is already renewable, electricity consumers are fully exposed to global gas markets.

The wiring is broken.

the receipts

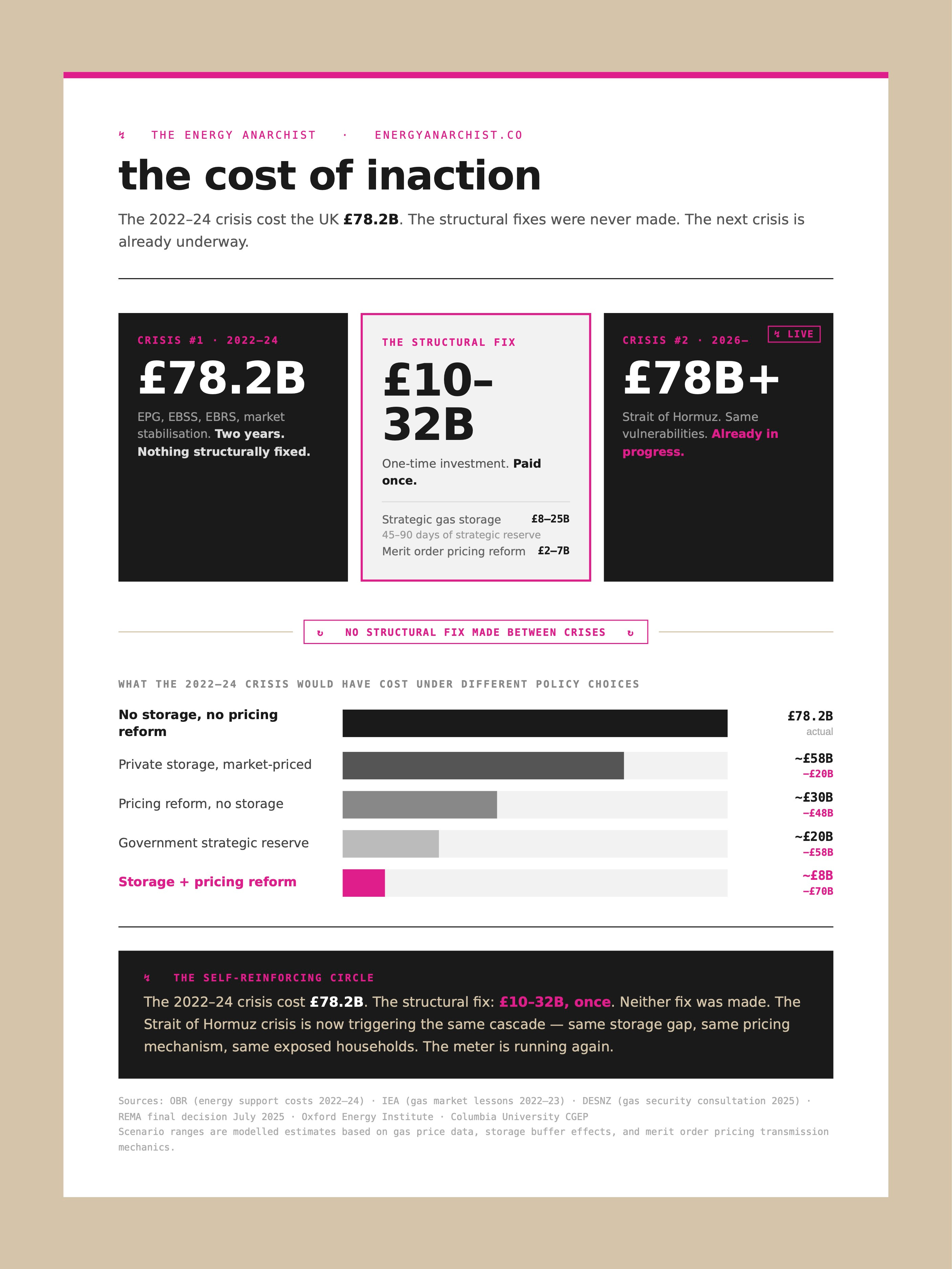

In 2022 - 24, the UK spent £78B managing the consequences of its energy policy. It’s safe to assume that the consequences of the US and Israel invasion of Iran will cost *at least* the same, because nothing has structurally changed.

The UK spends another £2.5B every single year on the permanent infrastructure of fuel poverty: schemes that exist because energy is structurally unaffordable for millions of households. It has also committed £17-18B over 5 years to make homes more efficient.

Not a single pound of that will buy the UK a more resilient energy system. We have consistently chosen to spend that money on managing consequences instead.

crisis interventions (2022-24 - reactive)

£78.2B (about 1.5% of GDP) spent purely on managing the consequences of structural failure (Source: OBR)

ongoing fuel poverty programmes (recurring, partially reactive)

£2.5B every year - the permanent costs of having structurally expensive, volatile energy. And yes, I know ECO’s been cancelled but I assume it has to be replaced with some other spend as part of the Warm Homes Plan.

forward-looking programmes (Miliband’s vision)

~£17-18B over 5 years… from a government in a perpetual and persistent cash crunch.

two case studies in wilful blindness

Storage.

Rebuilding Rough or its equivalent of ~3.3 bcm in storage would cost somewhere in the region of £2-3 billion. Of course, that still doesn’t get you close enough.

UK annual gas consumption is roughly 64 bcm and current storage capacity is ~3 bcm, so we need about 13 bcm of new build to hit Germany’s comparable 90-days.

Germany’s storage was built predominantly using onshore salt caverns and depleted onshore fields — the cheapest geology for this purpose, roughly £150-400M per bcm.

Sadly, the UK is not geologically blessed. Suitable onshore sites (Cheshire, Yorkshire, Teesside salt caverns) could realistically hold 5-8 bcm. Beyond that, you’re into offshore depleted North Sea fields which run closer to £500M-1B per bcm.

(Snam’s dCarbonX proposed 1.4 bcm facility is priced at roughly $1B, which tracks to that range.)

A realistic blended programme (onshore where geology allows, offshore for the rest) puts a full 90-day UK build at £15-25B over 10-15 years.

It’s genuinely harder for the UK to achieve 90-days of storage than it is for Germany; there’s a real physical constraint, not just a political excuse. A more achievable target (say 45-60 days) would cost roughly £8-12B and would still represent a transformation from the current position.

the inconvenient truth

The cynics (myself among them) will say that there would still be a crisis bill, even with 90-days of storage. And they would be correct. Let’s imagine the UK had 90-days worth of storage before the energy crisis:

Scenario A — Private storage, market-priced (current UK structure)

A private operator (e.g. Centrica) has no obligation to release stored gas at cost. They sell at market rates. The physical presence of 16 bcm would moderate panic and reduce some price pressure (studies on storage buffers suggest 20-30% price moderation in supply-constrained markets), but the spike still occurs.

At 25% lower average crisis prices (~£130/MWh vs £175/MWh):

Typical household bill: ~£3,300 instead of £4,200

EPG subsidy gap per household: £800 vs £1,700

Household bill support saving: ~£12-14B

Business support proportionally reduced: ~£3-4B saving

Total crisis cost: ~£55-60B. Saving: ~£18-23B.

Scenario B — Government strategic reserve, deployed at cost

If the government owns the reserve and releases gas at pre-crisis prices (which is the whole point of a strategic reserve) it can directly moderate market prices and reduce the subsidy gap.

At crisis prices moderated to ~£80-100/MWh (still elevated, but heavily buffered):

Typical household bill: ~£3,000-3,200

EPG subsidy gap: ~£500-700/household

Household bill support: ~£8-12B

Business support: ~£3-5B

Total crisis cost: ~£15-25B. Saving: ~£53-63B.

Even the top end of £25B spent over a decade is less than the £78B spent on the last crisis bailouts in two years, and we can assume this current one isn’t going to be cheaper.

But storage is not the full picture.

Pre-Ukraine war, Germany had 90 days of storage, filled to 90% capacity before the crisis hit, and still spent more than €150B on interventions. Why?

Pricing.

Storage doesn’t fix pricing. The gas price spike still transmitted to electricity prices for every unit consumed, regardless of where the gas came from. Having the storage gave them physical security but the market mechanism still amplified the price shock into every household bill.

This is where the UK’s actions have been particularly egregious.

The UK has some of the highest electricity prices in the world, and the ‘spark gap’ (the ratio of electricity to gas prices for consumers) is the highest among 25 large economies.

It’s an affordability and an economic problem. Energy UK found that almost 90% of companies have seen energy bills rise over the last 5 years and four in 10 had reduced investment as a result.

In July 2025, the government concluded the Review of Electricity Market Arrangements (REMA), a multi-year, multi-hundred-page examination of exactly why UK electricity prices are so volatile and so disconnected from the actual cost of generation.

The review identified the problem with precision. It then decided not to fix it.

Marginal pricing was explicitly examined and explicitly retained. The government’s reasoning centred on transition risk: changing the pricing structure would be complex and disruptive.

This is true. Independent analysis estimated the costs of reform to be £2-£7B:

System and IT changes (trading platforms, settlement systems via Elexon): ~£500M–£1.5B

Transition support / stranded asset compensation for affected generators: £1–5B depending on reform depth

Ongoing regulatory and operational changes: ~£100–200M/year

You know what’s also complex and disruptive?

Spending £78 billion on crisis bailouts every two years, and paying ~£2.5B every year to fund fuel poverty programmes, with essentially no measurable progress on improving fuel poverty.

The UK is not short of money. It is short of willingness to spend that money at the right end of the problem.

If the UK tackled both storage and pricing reform, we would spend about £32B and save ourselves about £70B in panic spending every time there’s an energy crisis.

(To be clear: by reform, I mean paying generators closer to their actual cost of production and passing consumers a blended rate, rather than pricing every kilowatt-hour as if it came from a gas plant.)

enter Miliband

To be fair to him: Ed Miliband didn’t build this mess. He inherited a system that was already structurally exposed.

Our manifesto is clear on this: energy systems are inherited, not chosen. No society votes its way out of an energy system overnight.

Miliband didn’t choose the starting point.

The problem is what he’s doing with the inheritance.

Pricing reform inaction is clearly on him.

Clean power by 2030 is the right destination. Offshore wind at scale, a revived nuclear pipeline, the end of new North Sea licensing… directionally, this is correct. The UK needs to get off gas. The long-term logic is sound.

But the manifesto is equally clear: targets are theatre, not strategy.

(as a reminder, here’s the full manifesto 👇🏻)

A target tells you where you want to be. It says nothing about how you function while you’re getting there. The UK will be running on significant volumes of gas through the mid-2030s regardless of what the 2030 target says, because energy infrastructure does not adhere to political timetables, because Hinkley Point C won’t come online until at least 2031, because the heating and transport systems being electrified are in the middle of a decade-long transition that can’t be accelerated by press release (oh, and no one can afford it).

During that window, every Hormuz-type event, every cold European winter, every Norwegian production outage hits the same structural vulnerabilities. The storage isn’t there. The pricing mechanism isn’t fixed. There’s no buffer.

More troubling than the timing gap is the category error. Judge energy by function, not virtue is the manifesto’s third principle, and it’s the one Miliband is most consistently violating.

The 2030 clean power target is a values statement dressed as a plan. Treating gas as the enemy of the transition, rather than the fuel that runs the transition, produces policies calibrated for the destination while ignoring the journey.

A system that collapses under stress is not liberating, no matter how virtuous its intent. Resilience — the manifesto’s highest principle — is not a feature of the 2030 plan.

a note on North Sea drilling.

The “open up drilling, cut bills” argument gets trotted out every time there’s an energy crisis, and it fails our manifesto test almost immediately.

UK gas trades at international prices. Domestic production doesn’t create a domestic price, so more North Sea gas does not mean cheaper bills. The UK isn’t Norway, which built Equinor, established a sovereign wealth fund, and created a domestic pricing structure specifically to capture national benefit from national resources.

The UK privatised everything and then was surprised when producers behaved like private companies.

There’s also the small matter of the windfall tax, which pushed total North Sea taxation to 75% and triggered explicit investment reductions from BP, Shell, Harbour Energy, and TotalEnergies.

You cannot simultaneously demand new long-cycle exploration investment and maintain a punitive, politically unstable tax regime. The two objectives are fundamentally incompatible.

(So is retaining expensive and volatile electricity pricing while demanding electrification and pinning your economic hopes on energy-intensive AI data centres, but that’s a discussion for another day.)

That said: the manifesto’s ninth principle is reject purity tests.

There is a narrow, honest supply security argument for the transition decade. The UK will burn gas for another 10+ years regardless. Marginal additional domestic production modestly reduces that exposure.

If you’re serious about it, fix the investment conditions, be honest about the timeline, and stop pretending it will cut bills. But it is one tool among several and it substitutes for nothing on the non-negotiables list below.

the non-negotiables

If Miliband is going to pursue a clean energy agenda (and he should) there is a minimum floor of structural fixes without which the agenda fails on its own terms.

These are not alternatives to decarbonisation, they are the pre-conditions for surviving it.

Strategic gas storage. Now, not eventually. The UK needs a buffer that can absorb a supply shock without triggering a national emergency. This is not a fossil fuel argument. It is a physics argument: the UK will burn gas for another decade at least, and burning it without a buffer is reckless.

Pricing reform. The REMA decision needs to be revisited. Reforming pricing is complex. It is less complex than explaining to people why electricity bills spiked again on a day when the grid was running 80% on wind, or budgeting £70-80B for energy crisis funding every 2 years.

A consumer transition mechanism that doesn’t require capital. Heat pumps, EV chargers, home insulation… the entire electrification pathway assumes households have £5,000-15,000 to invest. The households most vulnerable to energy are the least able to fund the transition. Without a financing mechanism that doesn’t require capital outlay, the clean energy agenda is structurally regressive.

(oh, what’s this? an option for funding?)

Dispatchable capacity. Wind and solar are the right answer for the long run. They are not dispatchable: they cannot be switched on when the grid needs them. The gap needs to be filled by something that can. That means nuclear, and it means Hinkley and Sizewell need to be treated as national infrastructure projects, not managed as procurement exercises.

the bill we’re about to get

The UK is not a poor country making hard trade-offs with limited resources.

It is a wealthy country that has consistently chosen to pay for the consequences of a broken energy system rather than fix the system itself.

Miliband’s direction is correct. His plan, as it stands, will deliver a cleaner grid in 2035, assuming everything goes to schedule, assuming no further supply shocks, assuming consumers can fund the transition, assuming Europe has surplus power available whenever the UK needs it.

None of those assumptions are safe. We live in a volatile world.

The energy anarchist position is not that clean energy is wrong. It is that energy is the operating system of civilisation, and you do not upgrade an operating system by announcing the target version while leaving the security vulnerabilities unpatched.

Fix the storage. Fix the pricing. Insure the journey.